Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When most people hear “reverse mortgage,” their guard goes up. They’ve heard stories, they assume the bank ends up owning the home, or they think it’s only for people in financial trouble. That reaction is normal-and honestly, it comes from old information and half‑truths, not how today’s FHA‑insured HECM actually works.

I want to give you a more complete picture, because for many financially responsible homeowners in their 60s and 70s, a HECM is less about “borrowing out of desperation” and more about using home equity in a controlled, tax‑efficient way to make retirement safer and more flexible.

1) First level: What it really is (and isn’t)

You still own the home. Title stays in your name; the lender has a lien, just like any other mortgage.

There are no required monthly principal and interest payments as long as you live in the home, keep taxes and insurance current, and maintain the property.

The loan is FHA‑insured and non‑recourse: you and your heirs can never owe more than the home is worth.

Your heirs inherit the home, not the debt. They can sell, keep, or walk away if the numbers don’t make sense.

Once people understand those mechanics-how the lender eventually gets repaid from the home’s value, and how FHA insurance fills any gap-the “too good to be true” alarm usually quiets down.

2) Second level: Why smart planners actually want this

This is where Brady Mullen’s thinking is helpful: the value is in how a HECM changes the sequence and timing of how you use your wealth, not just that it “gives you cash.”

Here are strategic uses that resonate with financially literate clients:

Smoother retirement income

Use a HECM line of credit so you don’t have to sell investments in bad markets; you can draw on home equity and give your portfolio time to recover.

That reduces “sequence of returns” risk-one of the biggest threats to a portfolio in early retirement.

Better Social Security and pension strategy

A HECM can provide cash flow that lets you delay claiming Social Security to get a higher lifelong benefit.

For couples, that can also increase the survivor benefit if one spouse passes away first.

Tax‑aware cash flow

HECM proceeds are loan advances, not income, so they’re generally not taxable and usually don’t affect Social Security or Medicare.

That means you can reduce taxable IRA withdrawals in high‑tax years and lean more on home equity instead.

Funding the right home for retirement

With a “HECM for Purchase,” you can buy a more suitable home (single‑level, closer to grandkids, lower maintenance) using part of your cash and part HECM, with no required monthly P&I payment.

This lets you preserve more liquid assets instead of tying everything up in a house.

Aging in place on your terms

Use equity to pay for in‑home care, safety upgrades, and modifications (ramps, baths, railings) that make staying put realistic.

That can delay or sometimes avoid a move into assisted living, which is often more expensive and disruptive.

This isn’t about “taking money from the house to splurge.” It’s about using home equity as a flexible, back‑up asset to protect everything else you’ve built.

3) Tax benefits and “maxing out” planning options

Used thoughtfully with your CPA/financial planner, a HECM can improve your after‑tax situation:

Non‑taxable cash flow

The money you receive from a reverse mortgage is considered loan proceeds, not taxable income.

That means you can supplement lifestyle spending without pushing yourself into a higher tax bracket or triggering IRMAA surcharges as easily.

Smarter withdrawal patterns

In high‑income years (big Roth conversions, business sale, RMDs, etc.), you can lean more on home equity and less on taxable account withdrawals.

Over time, that can extend the life of your portfolio and lower total taxes paid on retirement assets.

Interest deduction timing

Reverse mortgage interest generally isn’t deductible as you go; it becomes deductible (subject to IRS rules) when the loan is paid off.

In some cases, that creates a large itemized deduction in the year of payoff, which can be planned around other big tax events.

Capital gains context

When the home is eventually sold to pay off the HECM, normal capital gains rules apply-often with a large exclusion on primary residences.

Many sellers never even hit the taxable gain threshold once exclusions and improvement costs are factored in.

Bottom line: when you coordinate a HECM with your tax and investment plan, you’re often trading a single, illiquid asset (a fully paid‑off house) for more flexible, tax‑aware options.

4) Third‑order effects most people miss

This is where the “negative product” narrative really falls apart once people zoom out.

Protecting your other assets

By using housing wealth strategically, you may reduce the risk of running out of liquid money if you live longer than expected.

That can preserve more of your investment accounts for late‑life healthcare, long‑term care, or legacy goals.

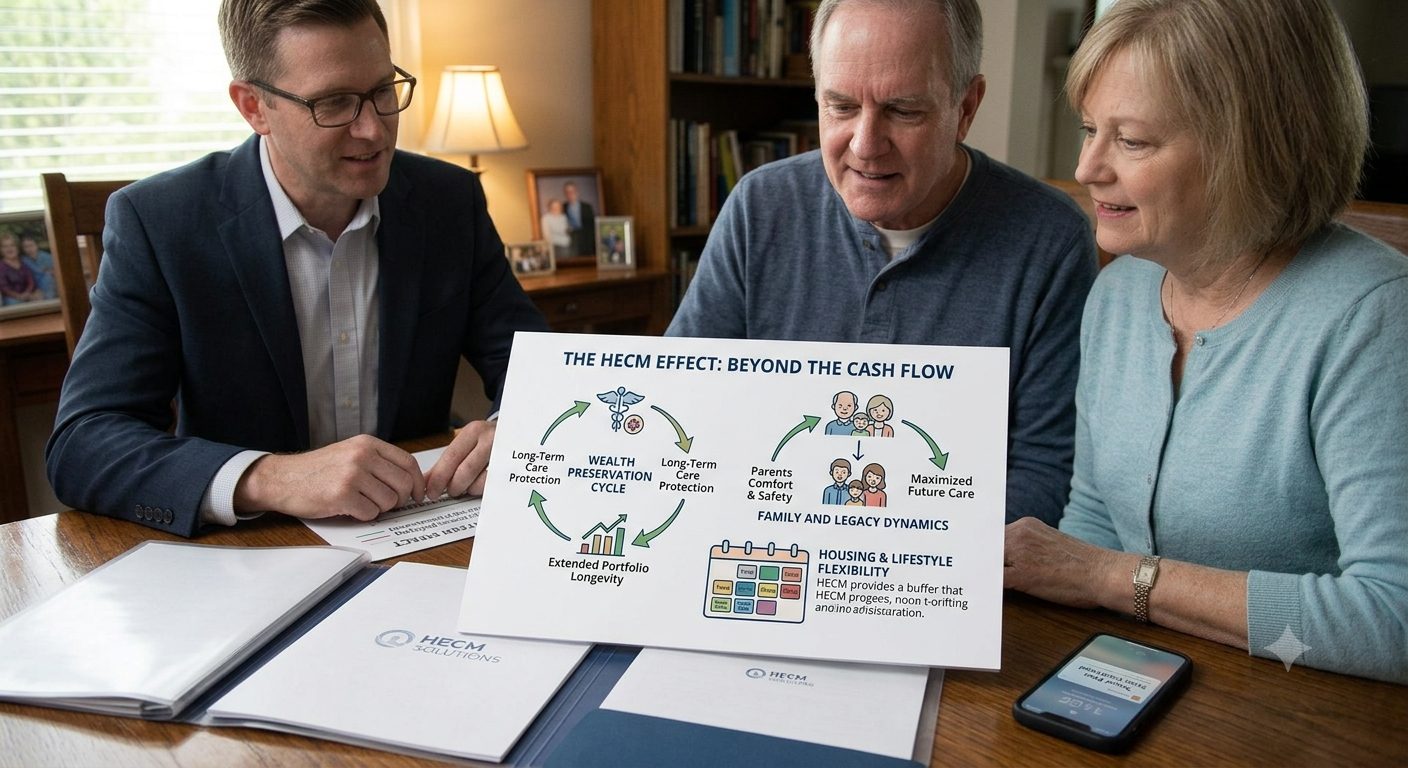

Family and legacy dynamics

Many adult children are more interested in parents being comfortable and safe than in maximizing inheritance, especially once they understand the safeguards and options.

In practice, kids often become advocates for a reverse mortgage when they see it relieves pressure on them and supports better care for their parents.

Housing and lifestyle flexibility

You’re not “stuck” in the house just because you took a HECM; you still have the option to sell, move, or downsize later.

Having that extra buffer can make decisions about travel, gifting, or helping family members easier without fear of “outliving your money.”

Psychological benefit: permission to spend

A lot of retirees under‑spend because they’re afraid of draining accounts too fast.

Knowing there’s a structured, FHA‑insured way to tap home equity can give you permission to use your wealth while you’re healthy enough to enjoy it.

5) What are the real downsides?

I don’t want to pretend this is perfect. There are trade‑offs:

Interest accrues over time, so your home equity will be lower in the future than if you never used a HECM.

There are upfront costs, similar to other FHA‑type loans, so it’s not ideal if you expect to move again in a few years.

You must stay current on property taxes, insurance, and basic upkeep, or the loan can become due.

For the right homeowner-someone who wants to stay in their home, has significant equity, and cares about risk management as much as inheritance-these downsides are usually acceptable relative to the extra flexibility and security they get back.

If you’re open to it, the next logical step is a numbers‑based review: looking at your home value, your existing savings, and your income plan to see whether a HECM strengthens or weakens your overall picture.

No pressure, just math.