Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Greetings.

Let’s skip the trade-press bullshit for a minute.

Normal people do not care about Zillow /Compass lawsuits, portal drama, or which brokerage bought which.

That’s the stuff agents argue about in Facebook groups when they should be learning how to negotiate.

You care about your timing, your money, and your next move.

So let’s get into the questions real Boulder homeowners are actually asking me, not the pretend ones we trot out for marketing scripts.

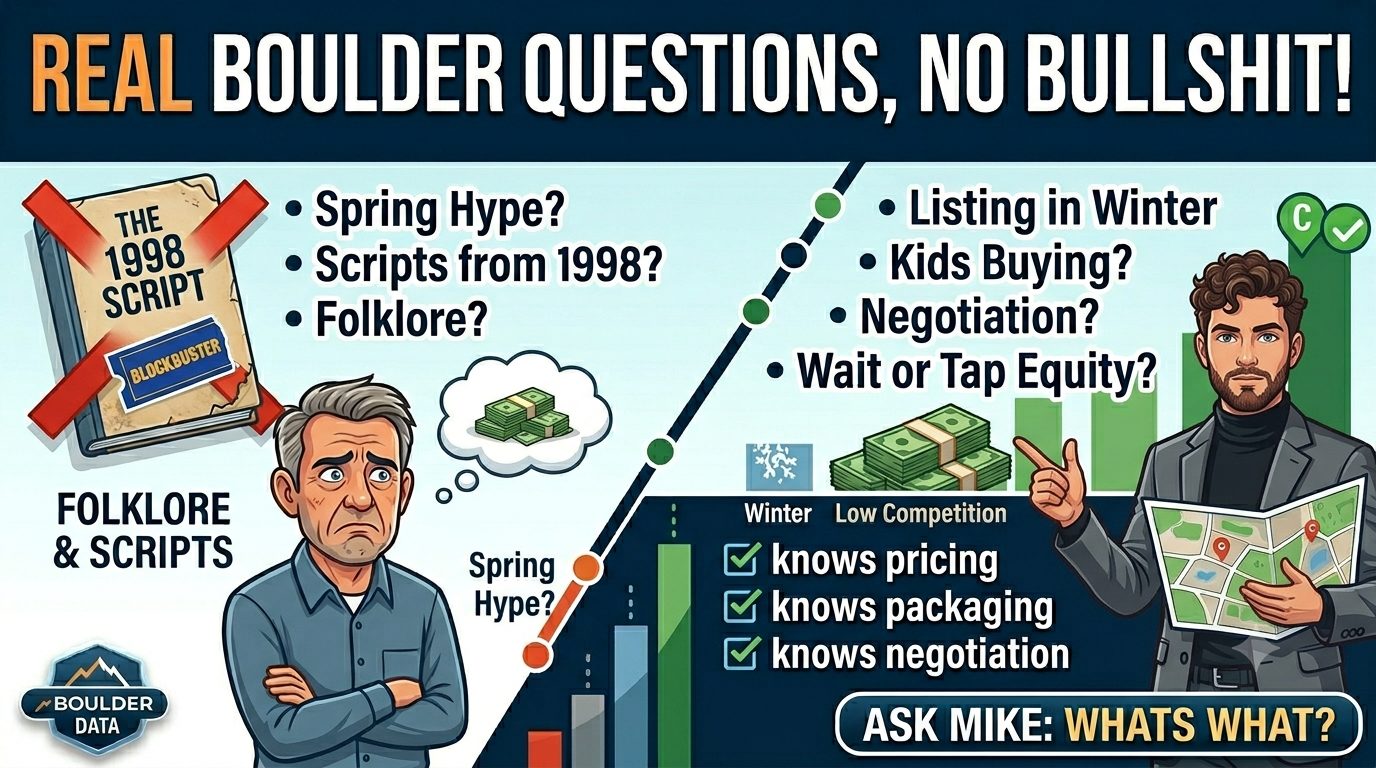

1. “When should we list to make the most?”

Most people think spring is the magical selling season.

It’s not. And if you’ve been reading my October and November emails, you know I’ve beaten the life out of this point already.

Spring = more inventory.

More inventory = more competition.

More competition = lower net.

The best time to sell is when inventory is low and buyers are serious, not when the tulips pop.

And yes, timing isn’t the same for everyone.

2. “Is the market crashing?”

Short answer: No.

What IS happening:

great inventory still sells instantly

bad inventory still sits

and the “just okay” listings are trading a full 10% below where they would’ve landed had they been packaged and launched correctly the first time

What’s also happening:

serious buyers win

unserious buyers complain

…and they complain about everything: sellers, agents, bankers, rates, paint color, take your pick.

And if I had a nickel for every guy who’s done one real estate transaction since 1999 telling me he’s “waiting for rates AND prices to come down,”

I’d sit in Decent Bagel all day drinking coffee.

Economists have a great line for this kind of fantasy thinking:

“Macroeconomists have successfully predicted nine of the last five recessions.”

Translation:

Nobody knows anything with certainty, especially not your uncle who bought his house for $210K in ’94.

3. “Will the market hold until spring while we get ready?”

Sure, but that does NOT make spring the smartest time to list.

And I’ll give you a hint:

Does waiting put more net in your pocket, or less?

Sometimes waiting gives you leverage.

Sometimes it lets your neighbors beat you to market and eat your lunch.

If you trust the person giving you advice, hire them.

But make sure they’re using data, not folklore.

4. “Why do agents all sound the same?”

Because most were trained on scripts from 1998 that should’ve been buried next to Blockbuster.

Most agents aren’t willing to have hard conversations at kitchen tables.

They’ve been trained to ‘get the ink’ and leave your home with a signed listing agreement.

They tell you what you want to hear at the listing appointment.

And then reality forces them to tell you the truth later.

I’d rather tell you the truth out the gate.

If we agree, cool, let’s rock and get this sold.

If not?, thanks for your time.

You need someone who:

knows how to price, knows how to package and launch a listing

knows how to negotiate

knows the money side and the emotional side

knows how to speak for you when stakes are high

and can absorb the stress of inspections or appraisal drama while you’re at home holding your spouse’s and kids’ hands saying, “It’s gonna be okay,” even if you don’t feel that way

That’s the job.

Not beige blazers and drone footage.

5. “How do I help my kids buy a home?”

This one is emotional.

And it’s real.

Our kids are facing a tougher housing environment than we ever did.

Here are the mechanics that actually work:

gift of equity

down payment assistance stacked with parental support

203k or renovation loans

co borrowing with a planned exit

using your HELOC as the bridge

using a HECM as a bridge

buying a 2 or 3 unit where rent offsets the payment

owner financing (yes, it’s real, and yes, it’s smart)

And here’s the hard part:

Helping your kids without accidentally blowing up your own retirement.

Most agents aren’t equipped to advise on the money side, they can tell you whether your couch “shows well”… but not whether your plan triggers a tax event, a liquidity trap, or a cash-flow disaster.

Talk to someone who understands:

lending

cash flow

wealth transfer

non-QM options

and knows some well qualified CPAs, planners, private lenders, non-bank solutions

(Not Chase. Not Wells. Ask me about the platform jockey circus sometime.)

You’re paying me a lot to manage your transaction, lean on that.

6. “Should I stay and tap the equity, or sell?”

Both paths are valid. No simple answer here.

The mistake is making the decision emotionally and then reverse engineering the math.

Here’s a risk almost no one talks about:

Sequence of Returns Risk:

This is the risk that the order of your portfolio’s gains and losses wrecks your retirement.

If you get bad market returns early in retirement while also withdrawing, your nest egg can crater even if the long-term average return is great.

It’s not the average that kills you, it’s the timing of losses relative to withdrawals.

Call it the retirement version of getting punched in the mouth before the bell even rings.

Why am I qualified to help you navigate this? Am I?

Not because:

I was on Wall Street for 25 years

I’m in my sixties and look it

I seem smart

I curse a lot

I “sound honest”

Nope.

I’m qualified because:

I’ve lived both ends, the expensive steakhouses and the dive bars.

I’ve made mistakes I’m still embarrassed to admit decades later, and I’ve turned those liabilities into assets for the people I serve.

That’s what experience actually is:

Living enough life to keep people from stepping on the same landmines that I’ve found.

Peace,

Mike

I have a handle on the current real estate markets here and now. Reach out and ask me whats what. Because I’m only suggesting to you what I’d hope you’d tell me if I needed to know it.