Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

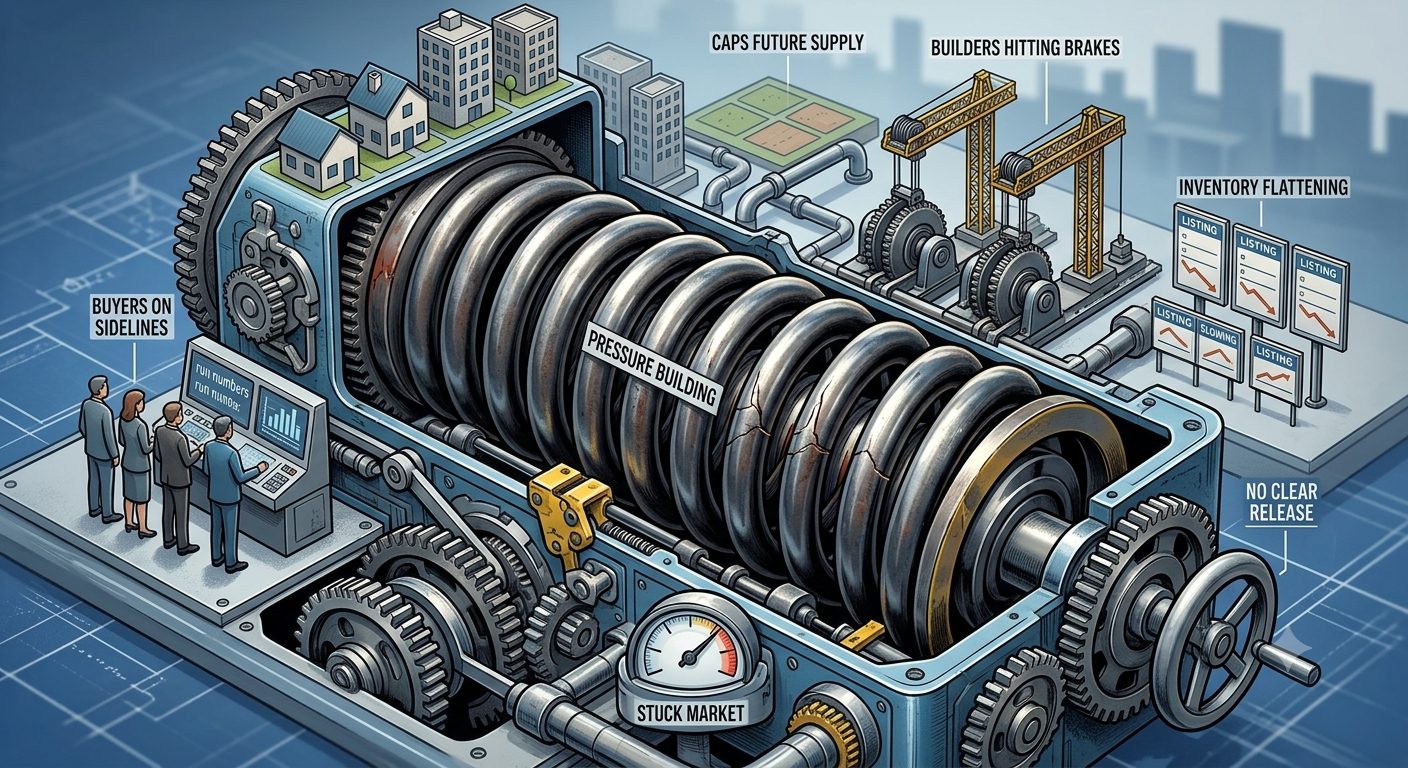

I keep coming back to the same image for this market:

It feels like a coiled spring.

Not a crash. Not a frenzy. Just a lot of pressure building with no clear release yet.

Here’s what’s actually happening under the hood:

Buyers have been waiting on “better rates” for almost two years instead of forcing payments that don’t make sense. They’re not gone; they’re on the sidelines running numbers.

Builders pushed a lot of product into the pipeline, but now they’re hitting the brakes hard, especially on apartments and condos, and dumping out what’s already under construction.

Because a lot of land is optioned instead of owned outright, they can walk away from future phases more easily than in past cycles, which quietly caps future supply instead of creating a fire sale.

New listings and overall inventory are not suddenly flooding the market. In many places, they’re flattening or slowing again.

So you end up with this odd mix:

lots of would be buyers, cautious builders, and no real surge in homes for sale.

Now overlay the macro picture:

Your 30 year mortgage rate is set by the bond market, not by a single person in D.C., but the bond market is watching the same movie we all are.

Over the last few weeks we’ve seen:

Strong labor data that keeps pressure on long term interest rates and makes the Fed talk about staying “higher for longer.”

A tentative U.S. Iran peace framework that’s cooled oil prices and nudged daily mortgage rate averages down a bit as markets start to price in slightly lower inflation down the road.

Those forces pull in opposite directions.

That’s what makes this feel like a coiled spring instead of a clear trend.

From here, there are really two main paths:

Path A: Rates ease, demand pops

In this path, the combination of cooling energy prices and softer inflation data eventually gives the bond market confidence that rates can move meaningfully lower.

What that looks like on the ground:

Mortgage rates drift down in a way buyers can feel in their payment.

People who have been on ice for 1-2 years suddenly step back in.

Builders are cautious and new construction hasn’t fully ramped back up, so supply doesn’t match the surge in demand.

That starts to feel a lot like a 2022‑lite replay in the “good” segments of the market:

more offers, less time to think, and nice properties getting bid up.

If you’re a buyer in a Path A world:

Being fully underwritten and ready before that wave matters more than trying to guess the exact week rates tick down.

The win is locking in the right asset (location, layout, time horizon) before competition re-heats, not perfectly bottom ticking a rate that you can maybe refinance later if the world really changes.

If you’re a seller in a Path A world:

You want to be positioned so that if demand does pop, your home is “first in line”: prepped, priced correctly, and live – not still in the planning stages.

The play is to capture renewed demand without assuming we’re back to 15 offer circus conditions on day one.

Path B: Rates stay sticky, turnover grinds lower

In this path, strong labor and sticky inflation keep pressure on long‑term yields. The Fed talks tough, and markets believe them.

What that looks like on the ground:

Rates bounce around but don’t truly break lower.

Existing owners stay put longer because giving up a sub‑4% mortgage for a 6‑ish percent one feels painful.

Turnover slows, the secondary market stays cautious, and the number of available homes never really expands.

You don’t get a crash, but you also don’t get a release valve. It’s a low‑volume, “stuck” market.

If you’re a buyer in a Path B world:

Patience and creativity start to matter more than chasing headlines. Off market opportunities, stale listings, and situations where terms matter more than price become real levers.

If your horizon is 7-10 years, waiting indefinitely for a perfect rate can cost you more in lifestyle and missed appreciation than it saves you in payment.

If you’re a seller in a Path B world:

The move has to be driven by your life, not by hoping for a return to 2021 pricing. I cannot stress this enough. Me and my family know life is short and act accordingly. Don’t let a balance sheet decision take over the lion’s share of your decision making. Does your house work for you know, cool, keep it……

If it doesn’t, and it adds stress to your life, your kids, your commute…..for god’s sake at least investigate what it would look like to materially change it now, in this next 12 months.

I know, who the f is this guy telling me to move?? Eff him. Yea I understand that. But I do speak from experience and honesty. I’m just suggesting humbly that maybe it might not be the circus you think it will be to set your squad up better.

So, the strategy shifts to: present a transition to a better home as the best option in a thinner set of choices, and make sure the buy side of your move pencils in a world where rates are “just okay,” not amazing.

So what should you actually do?

I don’t pretend to know exactly which path wins, and anyone who claims certainty here is guessing.

What I do know is that you don’t have to be a hostage to either outcome.

The right move is different if you are:

A buyer planning to be in your next home at least 5-10 years

A seller who knows you have a life driven move coming in the next 12-18 months

A homeowner who’s comfortable where you are but curious what options really look like in this kind of market

If you want to see how these two paths look specifically for your price point and neighborhood in Boulder / Broomfield / Erie, hit reply and just say:

“Spring”

I’ll send you a short, customized breakdown of what Path A and Path B would actually mean for your numbers, and how I’d position you so you aren’t boxed in either way.