Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Let me ask you a few uncomfortable questions.

Do you actually know how

Title insurance works in Colorado?

In most residential deals here, the seller pays for the buyer’s title insurance. That sounds great on the surface: “Free coverage, someone else pays.” But most buyers and sellers don’t really know what that policy covers, what it doesn’t, or that there are two different pieces to it.

There’s the standard owner’s policy (the “front” one most people know exists), and there are optional coverages and lender protections (the “back” end of the structure) that can make a real difference depending on easements, old liens, or quirks in the chain of title.

People will haggle over a $200 fee on a closing statement and never once ask, “Does this policy actually protect me from the weird stuff that could hurt me later?”

Now let’s talk HOAs.

Everyone knows dues are going up.

Everyone’s heard about insurance costs exploding in Colorado: hail, fire, wind, carriers tightening up or pulling out, premiums jumping. That’s the obvious, first level effect.

The second level effect is what worries me more:

Who is actually managing the impact of those changes?

Your HOA board is effectively a tiny government running a multi million dollar asset: buildings, roofs, garages, landscaping, insurance, reserves, capital projects. Most board members are volunteers with normal lives and jobs who stepped up because someone had to. Some are fantastic. Some are just overwhelmed.

Very few have real training in insurance, underwriting, long term capital planning, or vendor negotiation. Yet they’re making decisions that determine whether your building is properly insured, whether your dues go up 5% or 25%, and whether your reserves are healthy or headed for a special assessment.

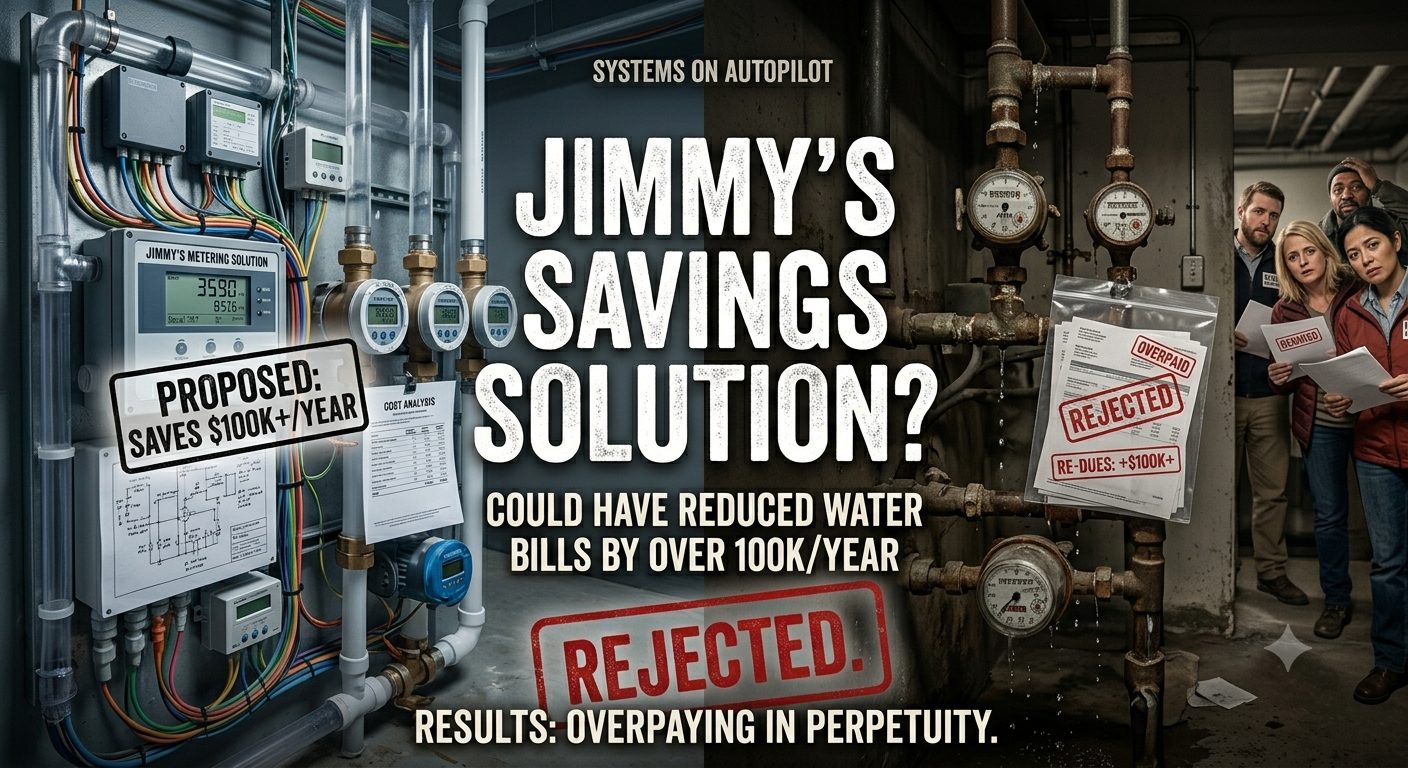

Here’s a real story:

A friend of mine, Jimmy, designs and installs metering systems for big apartment and condo projects. It’s his actual business. Before he moved out of his condo development, he brought his HOA a solution that would have reduced their water bill by over a 100k a year. He wasn’t trying to sell them his product; he was saying, “This exists in the market, here’s the math, go do this.”

They wouldn’t even seriously look at it.

The result? The building keeps overpaying for water every single year. Not because the technology doesn’t exist, but because the board didn’t have the time, interest, or structure to engage with it. And who pays that extra cost? Every owner, in perpetuity, through dues.

You see versions of this everywhere: in HOA decisions, in title choices, in how people handle their largest asset.

Here’s another example from a different world.

Recently, it took me two months to get in to see a specialist doctor. Several times I was asked, “Do you have your referral?” Several times I gave them the name and contact at my primary who had cleared it. I took the morning off work, prepped for a medical procedure, showed up… and the specialist said, “We still don’t have your referral. We should’ve had it yesterday.

Cool.

Remember when we spoke yesterday and I said call me if you can’t get it; I’m not taking the liability of the procedure on?

And to let me know because I can’t take the morning off to not get done what

needs to be done?

And also cool, thanks so much for availing me of “Would you like to reschedule now”?

No procedure, lost hours, and completely avoidable frustration.

On the plus side, I got to use all my tools this morning.🙄

This is what it looks like when systems are running on autopilot and nobody feels fully responsible for the outcome.

Now bring it back to real estate:

- Your HOA is running a multi million dollar budget, but very few owners ever read the insurance policy, reserve study, or capital plan.

- Your title policy is purchased for you, but most people don’t know what risks it actually covers.

- Lenders and the broader interest rate environment are dictating what you can and can’t do, but the strategy for you never gets beyond “I’ll wait until rates drop.”

On rates, here’s the short version:

Over the last four years, the 10-year Treasury (the benchmark that heavily influences mortgage rates) spiked from historic lows and then settled into a wide, choppy range. That’s why 30-year fixed mortgage rates ran up and have been bouncing around the mid-6s instead of “going back to 3%.”

Here is a picture of the last three and a half year’s of the US Treasury note rate from which your 30 yr mortgage rate is derived. What do you see? This is a box, there is no reason on gods green earth for the yield you see depicted to break out, up or down. Until there is of course.

Barring a genuine economic shock, there is no obvious catalyst sitting out there that suddenly drops us back into the world of ultra-cheap money. We are likely to stay in a broad band, think roughly high 5s to low 7s for a while.

Waiting for perfect might mean waiting forever.

If you’re renting and dropping serious money every month “until rates are better,” you’re making a bet that the future will be both cheaper and kinder than the present. Sometimes that’s true. A lot of the time, it isn’t.

Here’s the point of this whole rant:

You don’t need to become a title expert, an insurance underwriter, or a macroeconomist.

You do need somebody in the room who understands how these pieces work together and is willing to call BS on lazy systems and lazy decisions.

That’s the lane I stay in. And if you’ve been reading my stuff, you know I love to call bullshit.

I’m not here just to unlock doors and post pretty photos. I read the documents. I look at how the rate environment actually interacts with your cash flow and time horizon. And when I don’t fully understand a piece, I find or pay someone who does on your behalf, because my clients deserve that level of diligence.

Your home is not content for my social media. It’s the biggest line item on your balance sheet.

If you want to sanity check your current HOA, your title situation, or how today’s rate environment fits your plans for the next 3 – 7 years, hit reply.

I’m happy to take a look and tell you, candidly, whether you’re in good shape or if there’s something we should push on.

Peace