Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

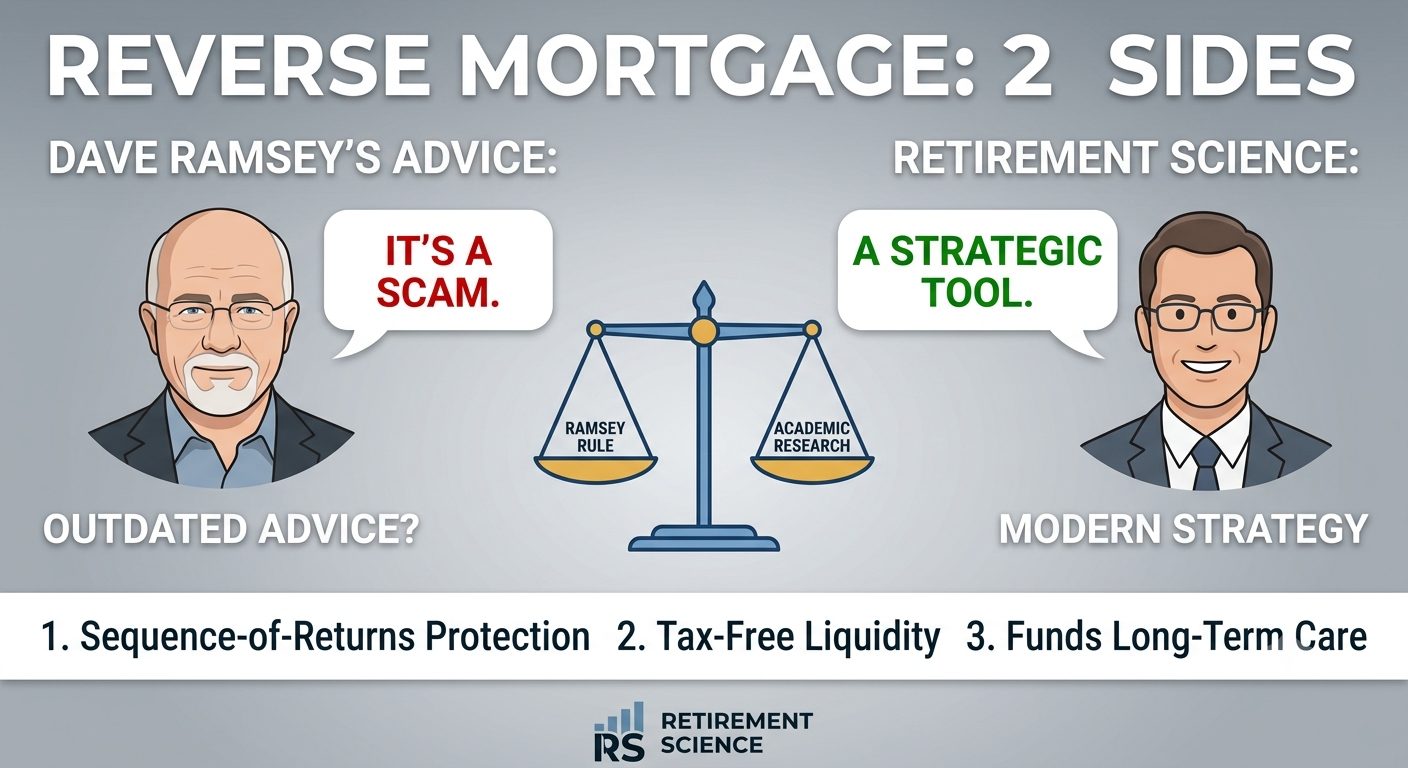

Every few months, Dave Ramsey repeats another blanket rule about mortgages, credit, or retirement.

His stance on reverse mortgages has always been crystal clear.

Across his books, videos, radio show, and website, Ramsey repeatedly says:

“Reverse mortgages are a scam.”

“Don’t do a reverse mortgage.”

“I would never recommend a reverse mortgage to anyone.”

“Reverse mortgages are dangerous and should be avoided.”

“You should NEVER take out a reverse mortgage.”

“If you have one, get out of it.”

That’s his right to believe.

But it’s not retirement science.

And it’s not current.

If you look at the actual research from the experts who study retirement risk, not radio personalities, the conclusions are very different.

Please don’t take my word for it.

Maybe take Wade Pfau’s and Barry & Stephen Sacks’.

Pfau (American College): https://tinyurl.com/2df9uj49

Sacks & Sacks (Journal of Financial Planning): https://tinyurl.com/3yuvv9b6

Here’s what the research shows, and what Ramsey never addresses:

1. Sequence-of-returns risk is the #1 retirement threat, not interest cost.

If markets fall early in retirement and you’re forced to withdraw from shrinking investments, you permanently reduce the lifespan of your portfolio.

Pfau and Sacks proved that using a HECM line of credit in down markets:

extends portfolio longevity 5-10+ years

preserves equity exposure

prevents forced selling

protects income stability

Ramsey never acknowledges any of this.

2. Set a HECM up early (age ~62) and the credit line grows smartly.

A $250,000 line of credit established at 62 commonly grows to:

$700,000-800,000 or even a $1,100,000mm by your 70s or 80s.

This growth happens:

even if your home value stays flat

even if your home value declines

It’s contractually built into every HECM.

This is not theoretical.

This is how the product works.

Ramsey never mentions any of this either.

3. You don’t have to liquidate a dollar of your retirement savings to set it up.

You can if you choose to, but it’s probably better to roll the cost into the mortgage.

No selling of assets at an inopportune time.

No penalties. No disruption.

And no RMD (required minimun distribution) shock, which is when the IRS forces you to withdraw from tax deferred accounts after age 73, sometimes pushing retirees into:

unexpected tax brackets

higher Medicare premiums

accelerated portfolio depletion

A HECM sidesteps the problem because:

HECM withdrawals are tax free and don’t count as income.

Tax-free liquidity, baby. Please show me how that is a bad thing. Please.

4. The biggest retirement expense isn’t a mortgage, it’s long term healthcare.

Dementia.

Alzheimer’s.

In home care.

Assisted living.

Surviving spouse longevity.

These are the real financial threats in retirement.

A HECM line of credit can pay:

taxes

insurance

maintenance

repairs

medical costs

in-home care

end of life care

Ramsey’s advice ignores the largest, most predictable expense retirees will ever face.

5. “You could lose your home!” is not a HECM risk, it’s a homeowner risk.

Ramsey warns that failing to pay taxes, insurance, or upkeep could cost you the home.

I’ve got news for you:

You lose your home for those reasons under EVERY mortgage.

Conventional, HELOC, free and clear ownership; it doesn’t matter.

The irony?

A smart household uses the HECM itself to pay taxes, insurance, and upkeep for life.

That’s not danger. That’s insulation.

6. The kids don’t lose out and they rarely want the house anyway.

What heirs usually want is:

liquidity

simplicity

flexibility

the absence of debt

the absence of deferred maintenance liability

A HECM gives them exactly that.

Leftover equity is theirs.

And here’s the part Ramsey never mentions:

7. A HECM is 100% non-recourse

If the loan balance ever exceeds the home’s value:

Neither you nor your kids owe a dime. Ever.

The FHA insurance fund absorbs the loss.

That’s why the product carries a cost, because it protects the borrower, not the lender.

Find me another financial tool where the government eats the downside and you keep the upside.

Here’s the heart of it:

The people who paid off their homes did the right thing.

They were disciplined. They were smart.

But the next smart step, the step Ramsey has never updated, is this:

Learning how to strategically leverage the equity you built to protect yourself and your family.

A fully paid-off home is great. A fully paid off home that also provides tax free, compounding liquidity is better.

A fully paid off home that protects your portfolio, funds long-term care, safeguards a surviving spouse, and carries very limited personal liability?

That’s modern retirement planning.

8. Bottom Line

Ramsey’s mortgage discipline is admirable.

His reverse-mortgage advice is outdated.

You deserve better than 1990s era talking points.

You deserve strategies backed by research, math, and reality, not slogans.

If you want to see how this works with your actual numbers, ask me to run it for you.

No pressure. No assumptions. Just clarity.